Inspiring Action With Visual Storytelling

How an empathy-driven narrative secured executive funding for a new Payments initiative at Citizens Bank.

Company

Citizens Bank

My Role

AVP, Senior UX Designer

Tools

- Sketch

- InVision

- PowerPoint

- Stock Photography

Problem

The Payments product organization possessed a robust strategic roadmap but lacked the narrative vehicle to secure executive buy-in and funding. Cross-functional alignment was stalled by dense, uninspiring documentation that failed to translate product vision into compelling business value for the executive committee.

Process

- Voice of the Customer Synthesis

- Persona Development

- Collaborative Design Workshops

- High-Fidelity Concepting

- Interactive Narrative Strategy

Outcome

Deployed an emotionally resonant visual storytelling framework that translated complex strategy into clear executive impact. This intervention secured Tier-1 funding from the Consumer Bank and accelerated priority sign-off from the Head of Digital Banking.

Background

As the AVP, Senior UX Designer for the Payments organization at Citizens Bank, I was responsible for shaping the experience roadmap for our consumer card and digital payments portfolio. Our team had a clear strategic vision, a disciplined backlog, and strong conviction about what the next generation of the Citizens Bank mobile banking experience should feel like for a modern customer.

What we did not yet have was executive funding. Without it, none of the work would ship. The roadmap, the research, the concepts, and the business case for the program all lived or died based on whether we could move the executive committee to say yes.

The Buy-In Problem

Securing funding inside a large regional bank is rarely a matter of producing better spreadsheets. Our leadership saw dozens of investment requests every quarter, each one backed by financial modeling, competitive benchmarks, and risk assessments. Dense documentation was the baseline expectation, not the differentiator. The real bottleneck was empathy. Most proposals described a customer segment in abstract terms and left executives to do the emotional work of imagining what life was actually like for that person.

I made a deliberate bet that visual storytelling could close that gap. If the executive committee could see and feel the customer we were designing for, the strategy would stop reading like a line item and start reading like a responsibility. Stakeholder empathy, built through imagery and narrative rather than prose, became the core tool I used to translate our roadmap into funded work.

The approach that follows is the exact narrative I walked stakeholders through. It begins with a single customer, a young professional named Mike, and it uses curated stock photography to ground every strategic decision in a human moment the room could recognize.

Building a Persona to Anchor the Story

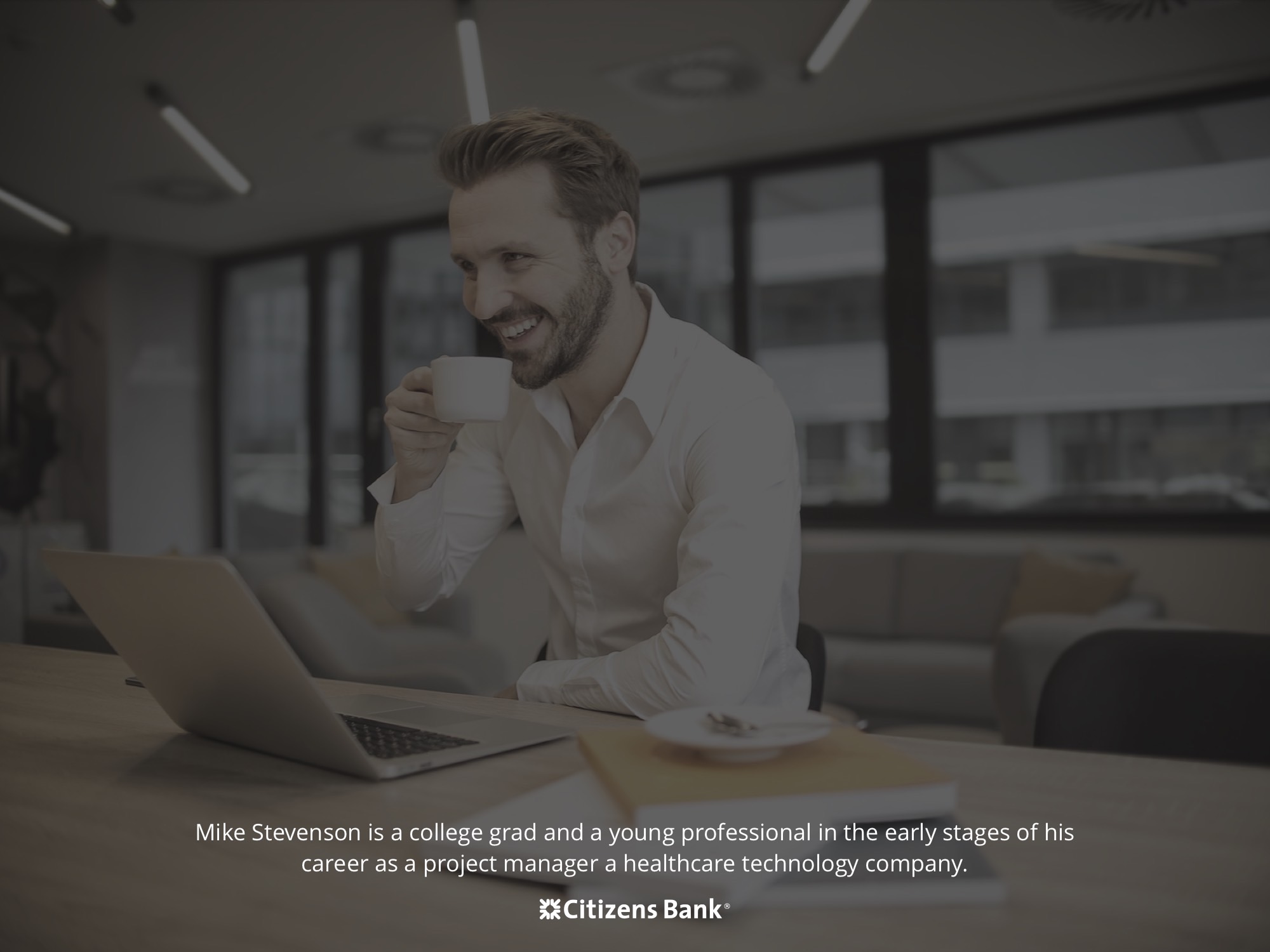

Before I could tell the story, I needed a protagonist. I developed a primary persona grounded in voice of the customer research, segmentation data from the Consumer Bank, and qualitative insights from in-branch interviews. The result was Mike Stevenson, a twenty-six year old project manager in Boston who represented the high-value, digitally native customer we were losing to challenger banks and fintech competitors.

The persona artifact captured more than demographics. It documented his behaviors, frustrations, goals, the financial products he already owned, and the way his friends described him. Each element was selected because it would later pay off inside the narrative. When Mike complained about long checkout experiences or having his identity stolen, those details were not decoration. They were the foundation for the product decisions the executive committee would eventually be asked to fund.

Meet Mike

With the persona established on paper, I needed to bring Mike into the room. I introduced him with a single full-bleed photograph: a confident young professional mid-stride in a modern urban environment, phone in hand, moving through his day with intention. No bullet points, no charts, just a person.

The moment landed because it reframed the conversation. Executives were no longer being asked to evaluate a segment. They were being asked to consider a specific human being whose financial life we had the privilege of supporting. That reframing set the emotional register for everything that followed.

A Day in Mike's Life is Already Full

The next beat of the narrative showed what Mike carries with him before he ever thinks about his bank. He is balancing deadlines at a health insurance technology company, planning a wedding, managing student loan debt, and trying to make thoughtful financial decisions in the margins of an already demanding day.

I used this section to make a point that is easy to forget inside a bank. Financial services are never the main event in a customer's life. They are the infrastructure that either supports or interrupts everything else. If our product demanded more attention than it returned, Mike would leave. Every design decision downstream would be measured against whether it respected the limited bandwidth he had to give us.

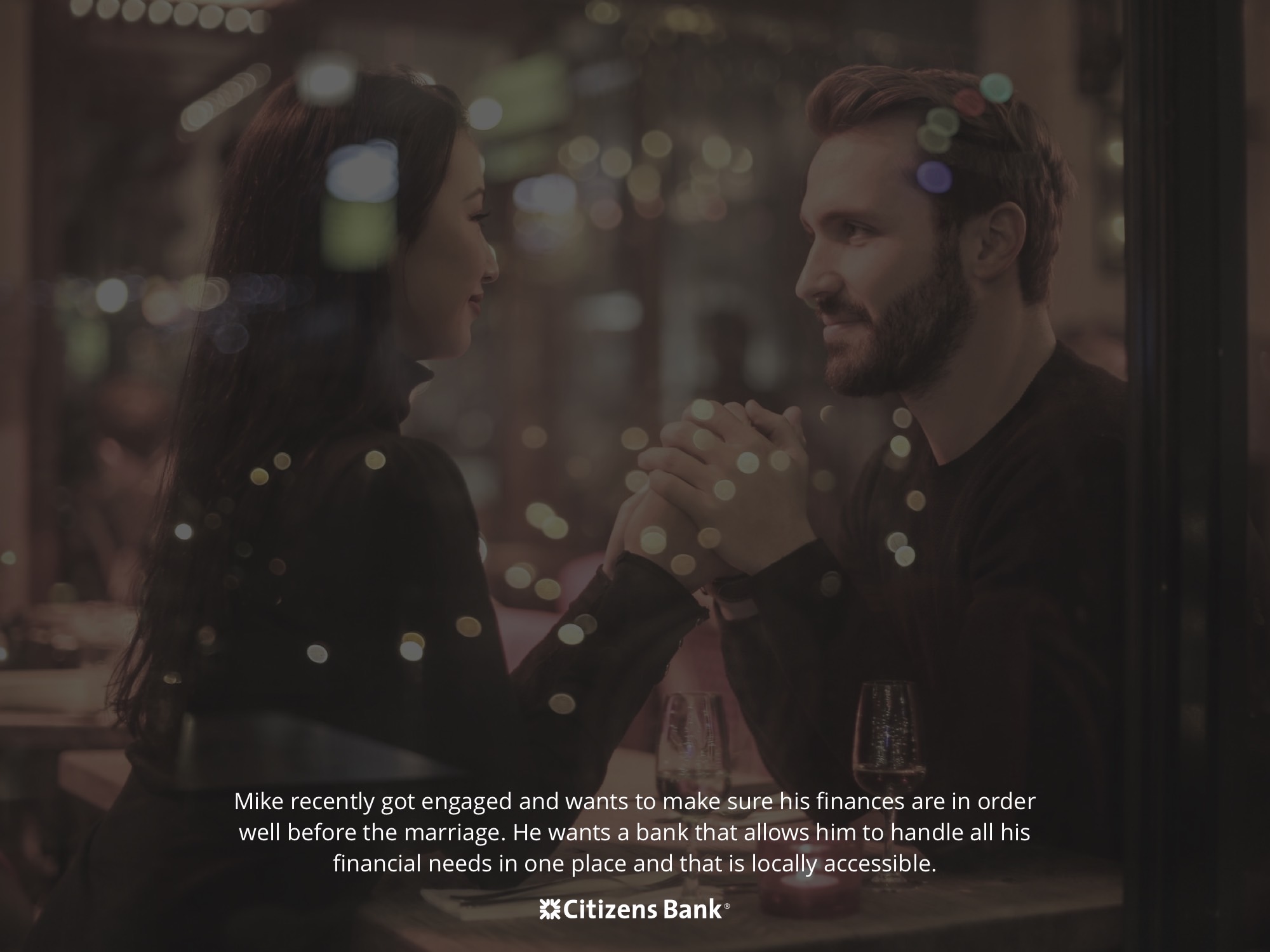

Mike Just Got Engaged

The next beat of the narrative introduced a life event that reframed everything. Mike recently proposed to his fiancée, and the two of them are now beginning the quiet, practical work of building a shared financial life. A wedding is on the horizon, a joint household is forming, and decisions that used to belong to one person are now being made by two.

That change created a very specific banking need. Mike is looking for a financial institution that can handle the full picture under one roof, checking, savings, cards, and the products that will come next, and one that is locally accessible to both him and his fiancée as they settle into their life together. Convenience and consolidation are no longer preferences for him. They are requirements.

This moment is where the room began to lean in. An engaged young professional choosing a primary bank is one of the highest-value acquisition opportunities in consumer banking, and the decision window is narrow. Winning Mike now meant earning a relationship that could compound across decades of life events.

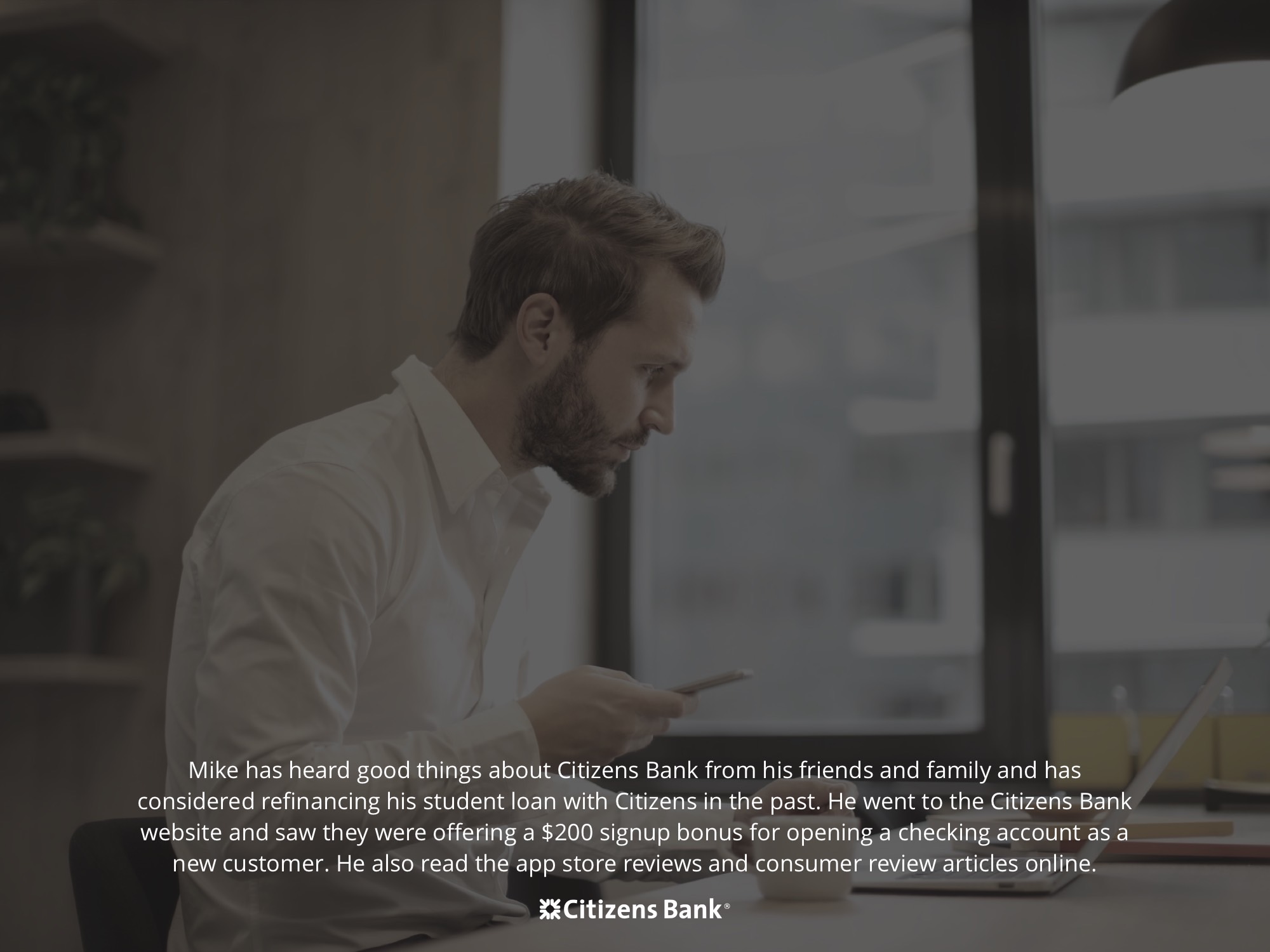

The Moment Mike Discovers Citizens

Every customer relationship begins with a decision, and I wanted the committee to feel the weight of that decision from Mike's side of the table. Mike discovers Citizens the way most modern customers discover any financial product: through a combination of digital research, peer recommendations, and a passing impression of the brand in his neighborhood. By the time he is considering us, he has already compared rates, read reviews, and quietly eliminated half a dozen alternatives.

Framing discovery this way raised the stakes on first impressions. The visual design of our marketing surfaces, the clarity of our product pages, and the tone of the onboarding flow were no longer marketing concerns. They were the opening move in a relationship we might only get one chance to start.

Walking Into a Citizens Branch

Even for a digital-first customer, the decision to open a new checking account often begins in the physical world. I showed the committee a photograph of Mike approaching a Citizens branch on foot, a familiar urban moment that grounded the abstract idea of acquisition in a recognizable street corner. The branch is still the front door of the relationship for a meaningful share of our customers, and the design of what happens on the other side of that door shapes everything that comes next.

This image also gave me a clean transition. It let the narrative move from the outside world into the branded environment where our people, our product, and our digital experience needed to work together as a single system.

Inside the Branch

The relationship begins the way it has always begun at Citizens, with a banker. Mike is greeted, seated, and walked through his options by a real person whose job is to understand what he and his fiancée actually need. The in-person conversation is still the emotional anchor of the experience, and the narrative deliberately preserved that.

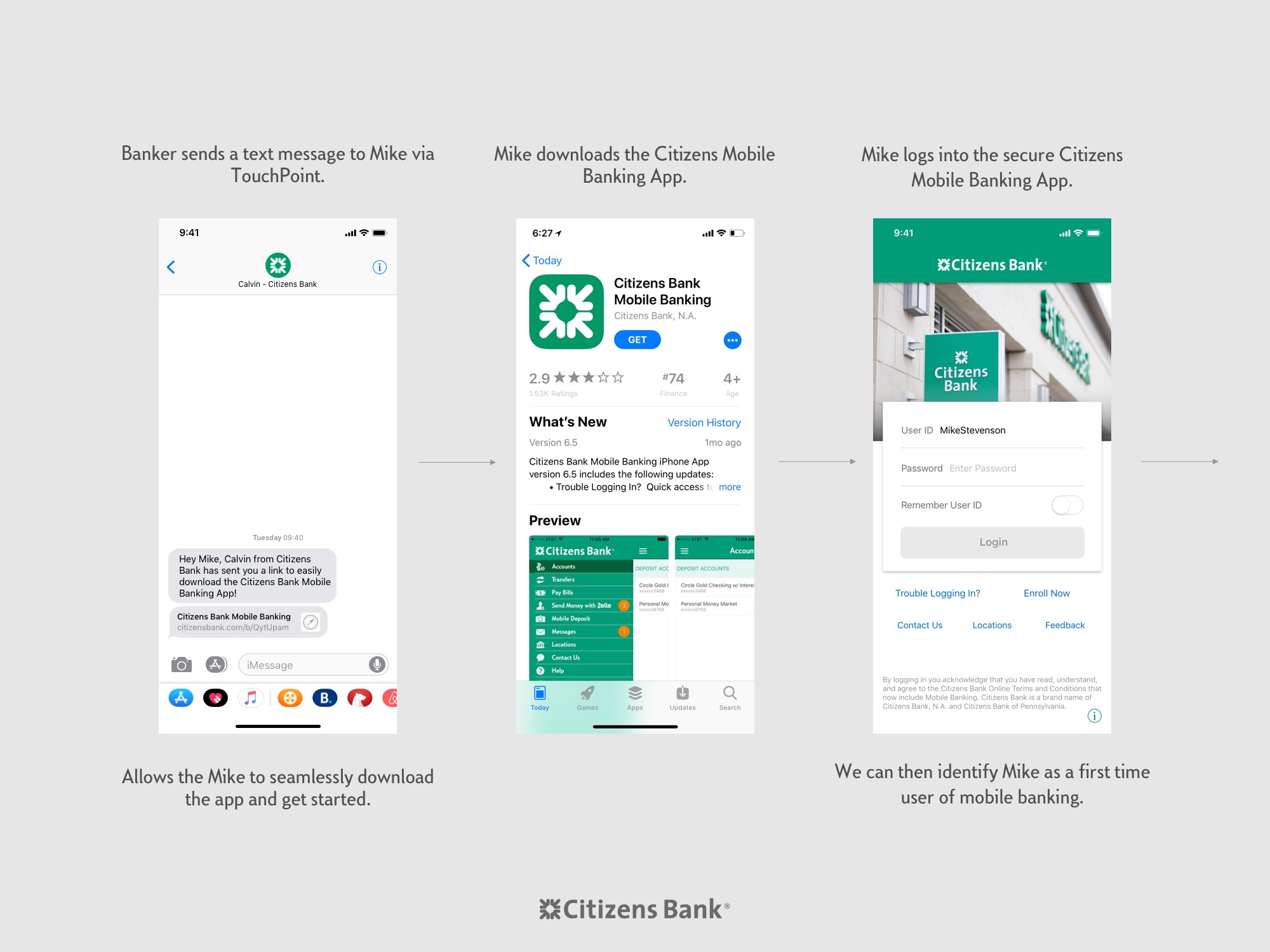

What changed in my proposal was how that conversation ends. Rather than handing Mike a printed brochure and a set of instructions he is likely to lose by the time he gets home, the banker uses Touchpoint to send him a text message directly from the desk. That single text message is the handoff. It carries a trusted link from the banker Mike just met, and it opens the door to the App Store listing for the Citizens Mobile Banking app.

From there, the digital journey begins on Mike's own terms. He downloads the app in the moment, while the context of the conversation is still fresh, and takes his first steps into mobile banking with a secure login flow that recognizes him as a brand new customer. Because the handoff originated from a known banker inside the branch, we can identify Mike as a first-time user of mobile banking and tailor the experience accordingly.

This framing honored the work of our branch teams while making the case for a digital investment. The goal was never to replace the in-person relationship. The goal was to extend it, seamlessly, from the banker's desk into Mike's pocket.

Mike's First Login Experience

Still seated inside the branch, just steps from the banker who welcomed him, Mike opens the newly downloaded Citizens Mobile Banking app and begins his very first login. The narrative deliberately kept him in the branch for this moment. The banker is still nearby, the environment is familiar, and any friction Mike encounters can be resolved in seconds by the person who just handed him the experience.

I paired a photograph of Mike on his phone with early visual concepts for a redesigned first-run experience. That first login is the real handoff between the branch and the digital relationship, and it is the moment where a thoughtful product can turn a new customer into a confident one. This was the natural place for the narrative to pivot from empathy into solution, and it is where the funded product work began.

Setting Up Zelle and Cardless Cash

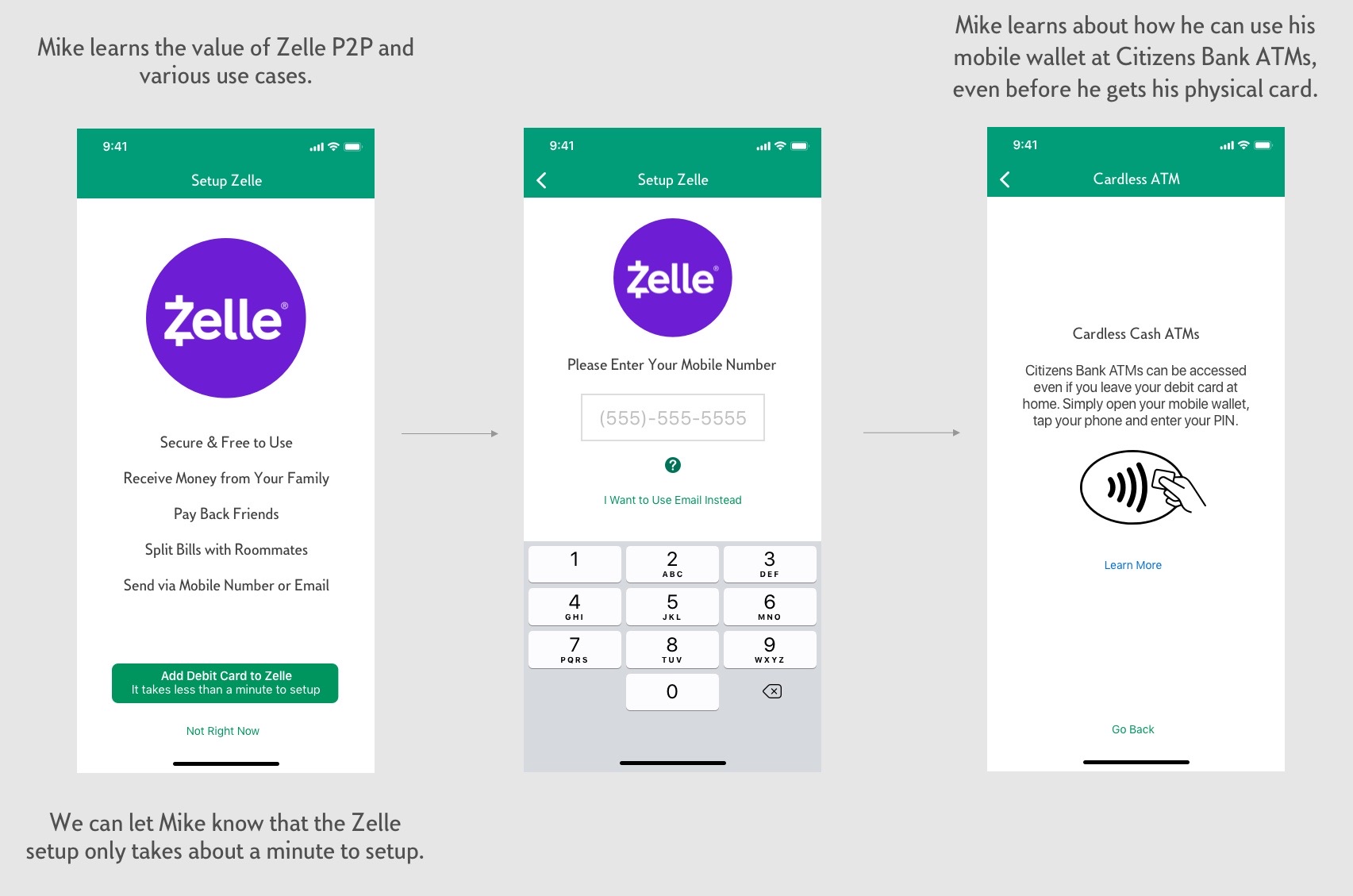

With his account provisioned and his first login complete, Mike is guided through the first of several high-value setup moments, all while he is still sitting inside the branch. The experience walks him through enrolling in Zelle for person-to-person payments and activating cardless cash so that he can withdraw money from a Citizens ATM using only his phone.

Placing these moments inside the branch was a deliberate strategic choice. A customer who enrolls in Zelle on day one becomes meaningfully stickier than one who defers the setup, and cardless cash is the feature that finally lets us close the gap between account opening and ATM access. The banker remains within arm's reach if Mike has a question, which turns what is often a frustrating self-serve flow into a guided, confidence-building experience.

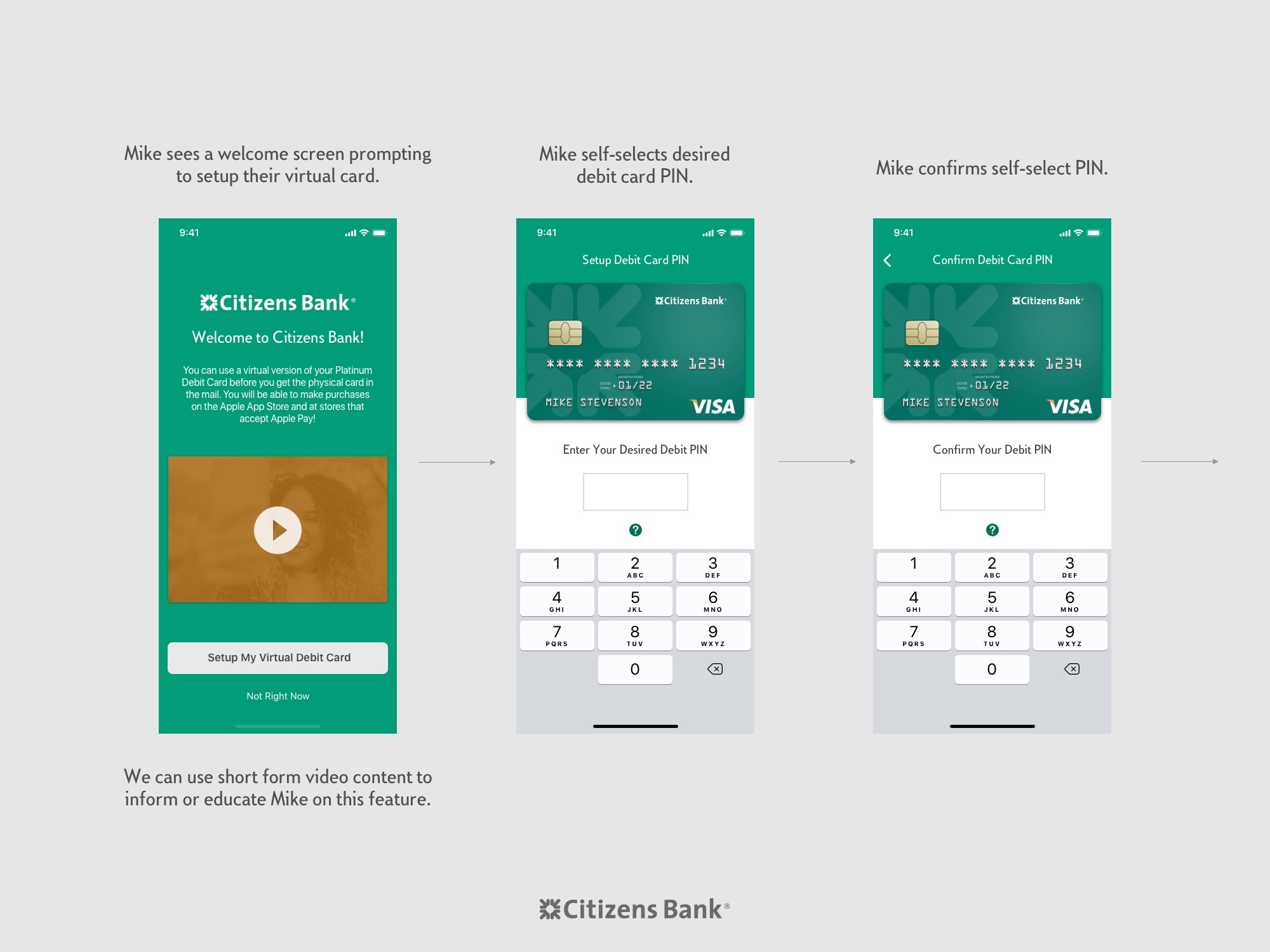

Self-Selecting a PIN and Provisioning Mobile Wallets

Still inside the branch, Mike continues through the guided onboarding flow and is invited to self-select the PIN for his new Citizens debit card. In the same experience, the app offers to provision his card to his mobile digital wallets, including Apple Pay, Google Pay, and Samsung Pay, so that he can begin transacting immediately without waiting for the physical card to arrive in the mail.

This section of the narrative emphasized a critical business insight. The days between account opening and the arrival of a physical card are the most dangerous window in the entire relationship, because they are the days a new customer feels like they have an account but cannot actually use it. Self-selected PINs and instant digital wallet provisioning collapse that window to zero, and the entire setup happens before Mike ever leaves his chair.

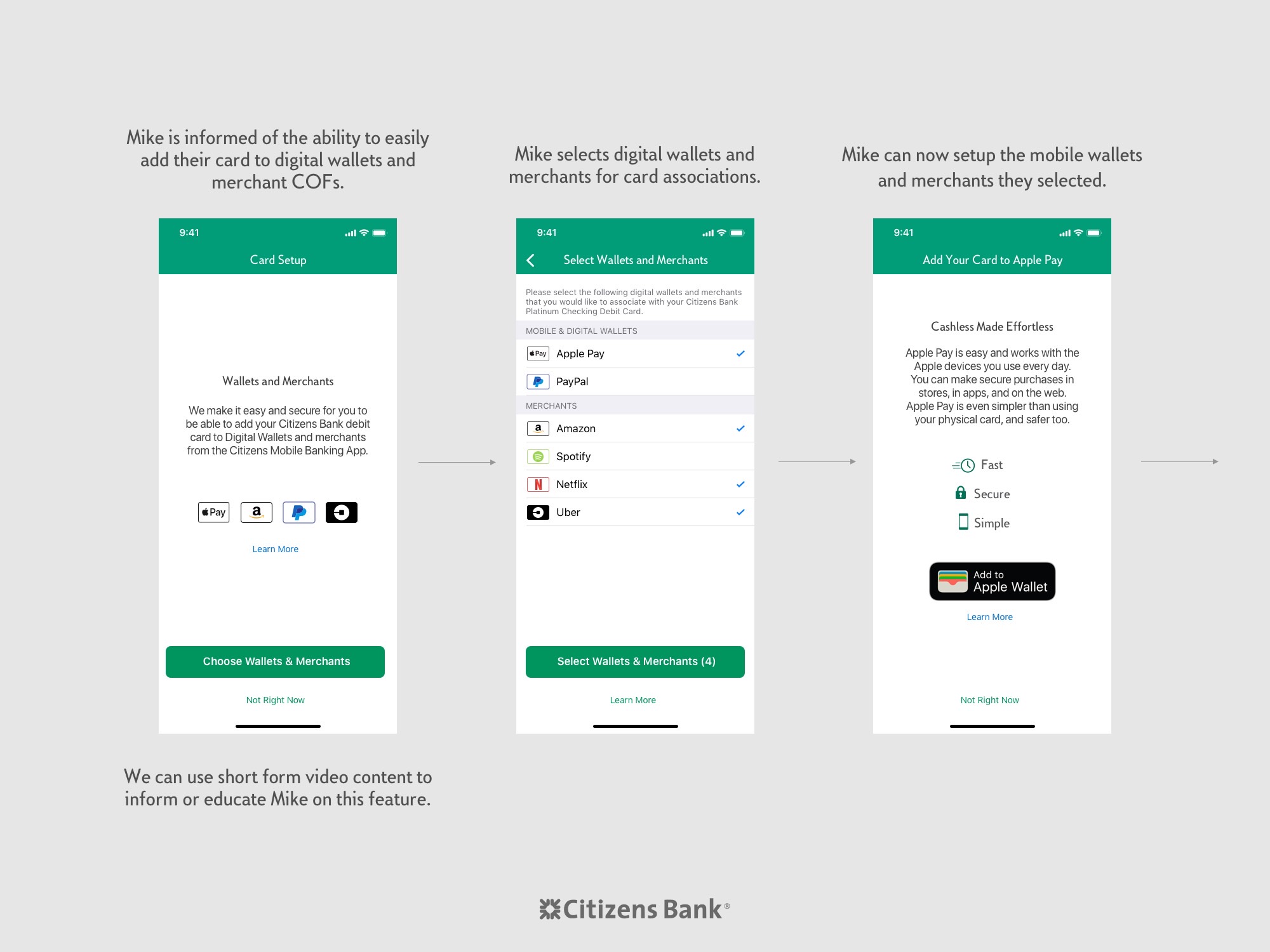

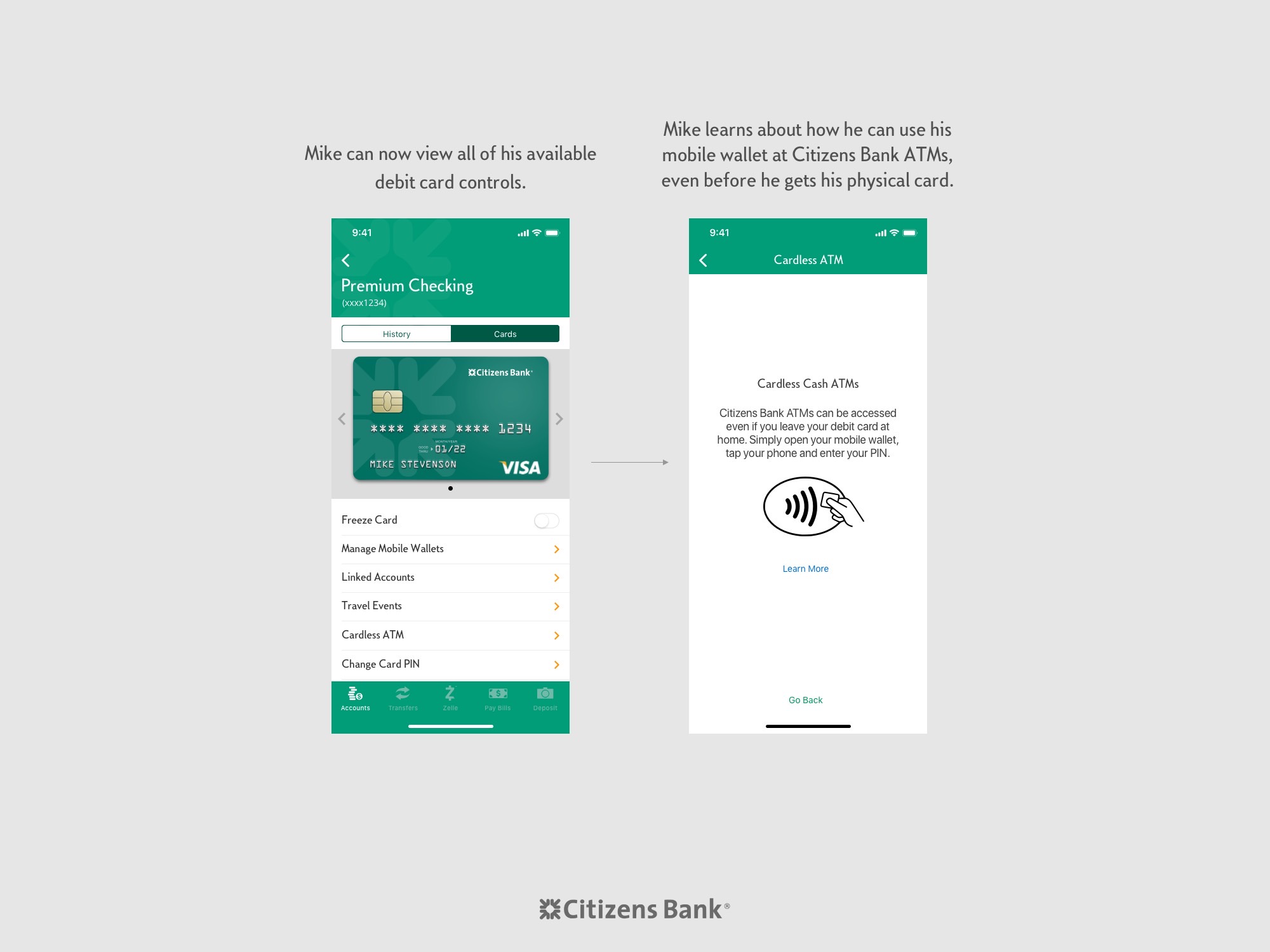

Card Controls and Cardless ATM Onboarding

The final step Mike completes while still inside the branch is the one that gives him the most control over his new account. The app walks him through setting card controls, including the ability to toggle his card on and off, set merchant category preferences, and configure alerts, and it activates the cardless ATM access that will let him withdraw cash from any Citizens ATM using only his phone. By the time this flow is complete, Mike has a fully armed debit relationship with Citizens and has not yet stood up from his seat.

I called out in the narrative that every one of these capabilities was already part of our technology roadmap. What this program was asking the executive committee to fund was not the underlying infrastructure. It was the integrated, empathetic experience that stitched those capabilities into a single coherent moment on day one of the relationship, before the customer ever left the branch.

Testing Cardless Cash on the Way Out

With setup complete, Mike finally stands up and begins to leave. On his way out, he stops at the ATM in the branch lobby to confirm that everything he just configured actually works. Using only his phone, he initiates a cardless cash withdrawal and completes his very first transaction as a Citizens customer, all without a physical card in his wallet.

This moment was the emotional peak of the narrative for the executive committee. Mike is technically still at the branch, but he is on his way out the door, and the product is already delivering on its promise. The ATM test turns an abstract feature list into a tangible proof point and converts the customer's last interaction with the building into a moment of confidence rather than uncertainty.

A First Apple Pay Purchase Across the Street

Mike leaves the branch and walks across the street to a local coffee shop. He orders a coffee, taps his phone at the reader, and pays for it with the Citizens debit card he provisioned to Apple Pay only a few minutes earlier. It is a small purchase, but it is the first transaction he makes in the world as a Citizens customer, and it happens before his physical card has even been printed.

I closed this part of the narrative on that image intentionally. Every preceding slide had been about the work Citizens needed to do to earn Mike's trust. This final moment showed the payoff. A young, engaged professional who just chose his primary bank is walking away from the branch with a fully functional debit relationship, a working mobile wallet, and a positive first transaction already behind him. For the executives in the room, that image made the funding decision feel less like a bet and more like an obligation.

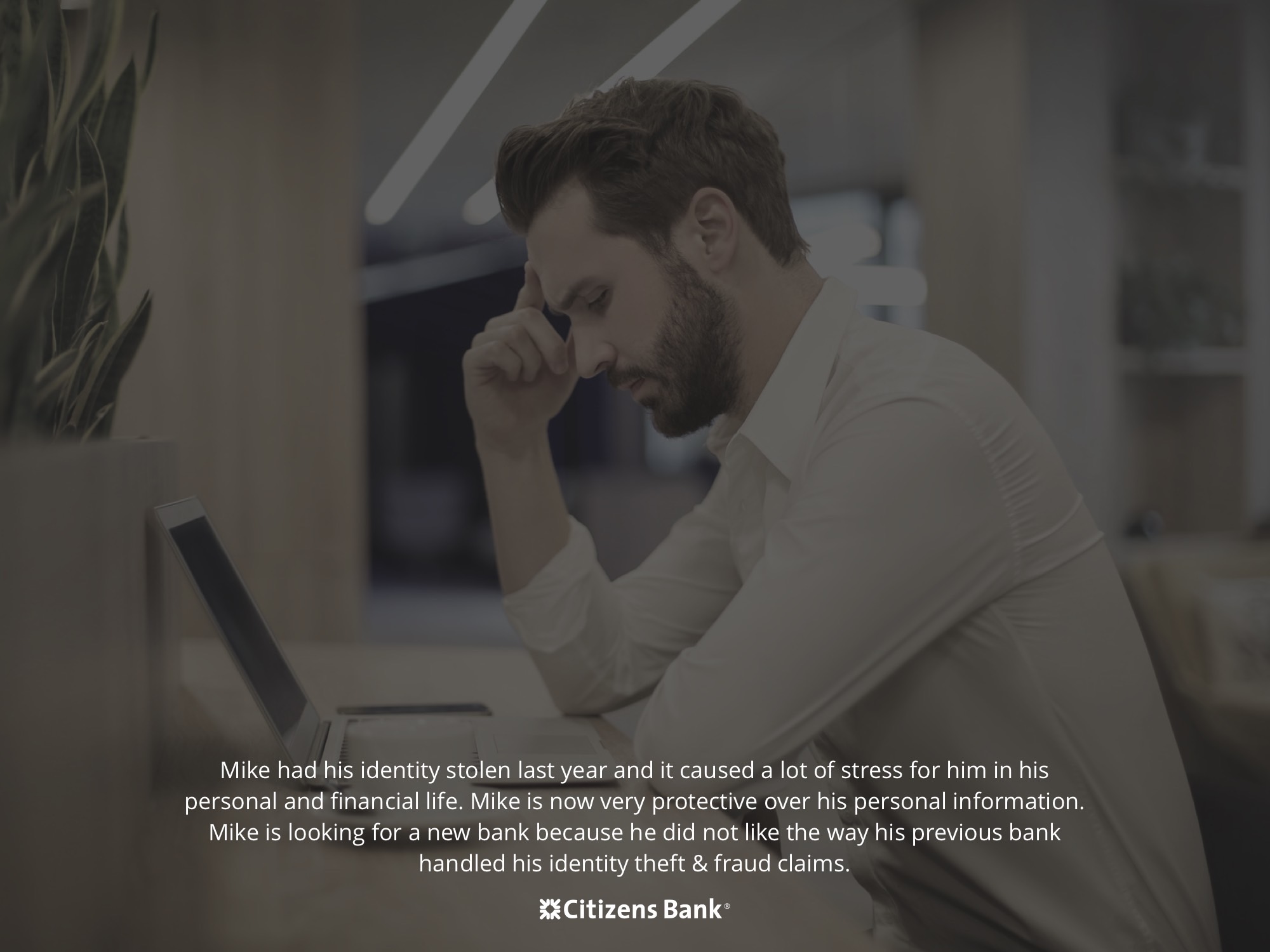

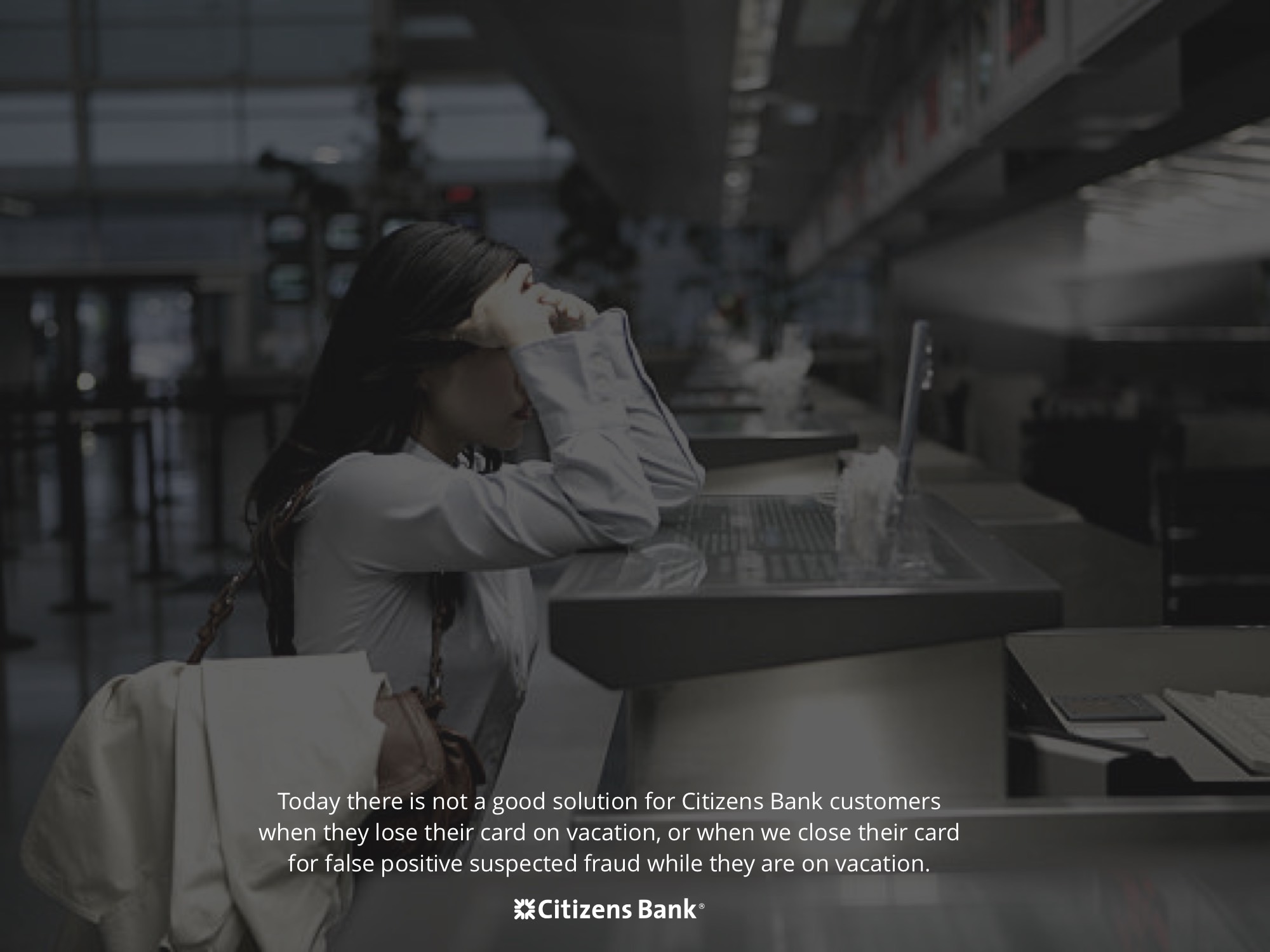

A Vacation Gone Wrong

With the executive committee now emotionally invested in Mike's onboarding story, I used the second half of the presentation to shift the narrative from a moment of delight to a moment of failure. This part of the story follows a different customer, one who has been with Citizens for years and is on vacation when everything suddenly goes wrong.

The setup is painfully familiar. The customer forgot to notify the bank about their travel plans, and their debit card is flagged and blocked the first time it is used outside their home region. Because the card has been closed for security, a replacement is automatically placed in the mail and sent to their home address. They are thousands of miles away, with a locked card, no backup, and no way to physically receive the new one until they return from the trip they are currently trying to enjoy.

The image of an upset customer on vacation was deliberately jarring. It pulled the room out of the Mike story and forced them to confront a scenario that most of them had either experienced themselves or heard about from a family member. Empathy had already been established. Now it was being redirected toward a problem that only a funded product investment could solve.

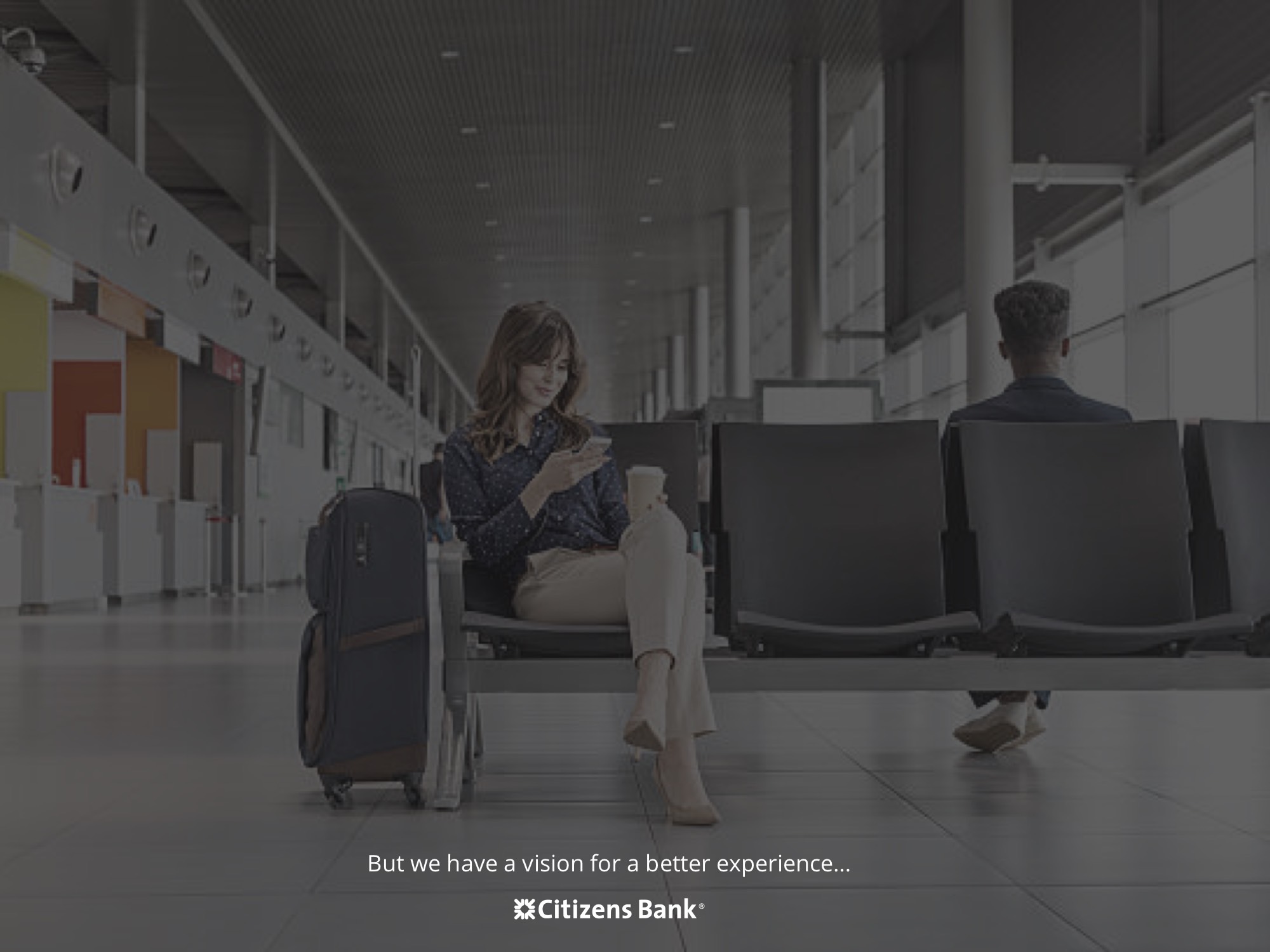

There Must Be a Better Way

After letting the weight of those customer voices settle in the room, I used the next slide to pivot the narrative one more time. The problem was real, the pain was documented, and the operational cost of the current experience was already being absorbed by our contact centers and social media team every single day. The obvious next question was whether Citizens could do something about it.

This slide was intentionally open-ended. It did not yet show the solution. It simply planted the belief that a better way was possible and positioned the rest of the presentation as the answer to a question the executive committee was now asking themselves. The solution concepts that followed this slide were the specific reason the program needed funding, and the room was finally ready to hear them.

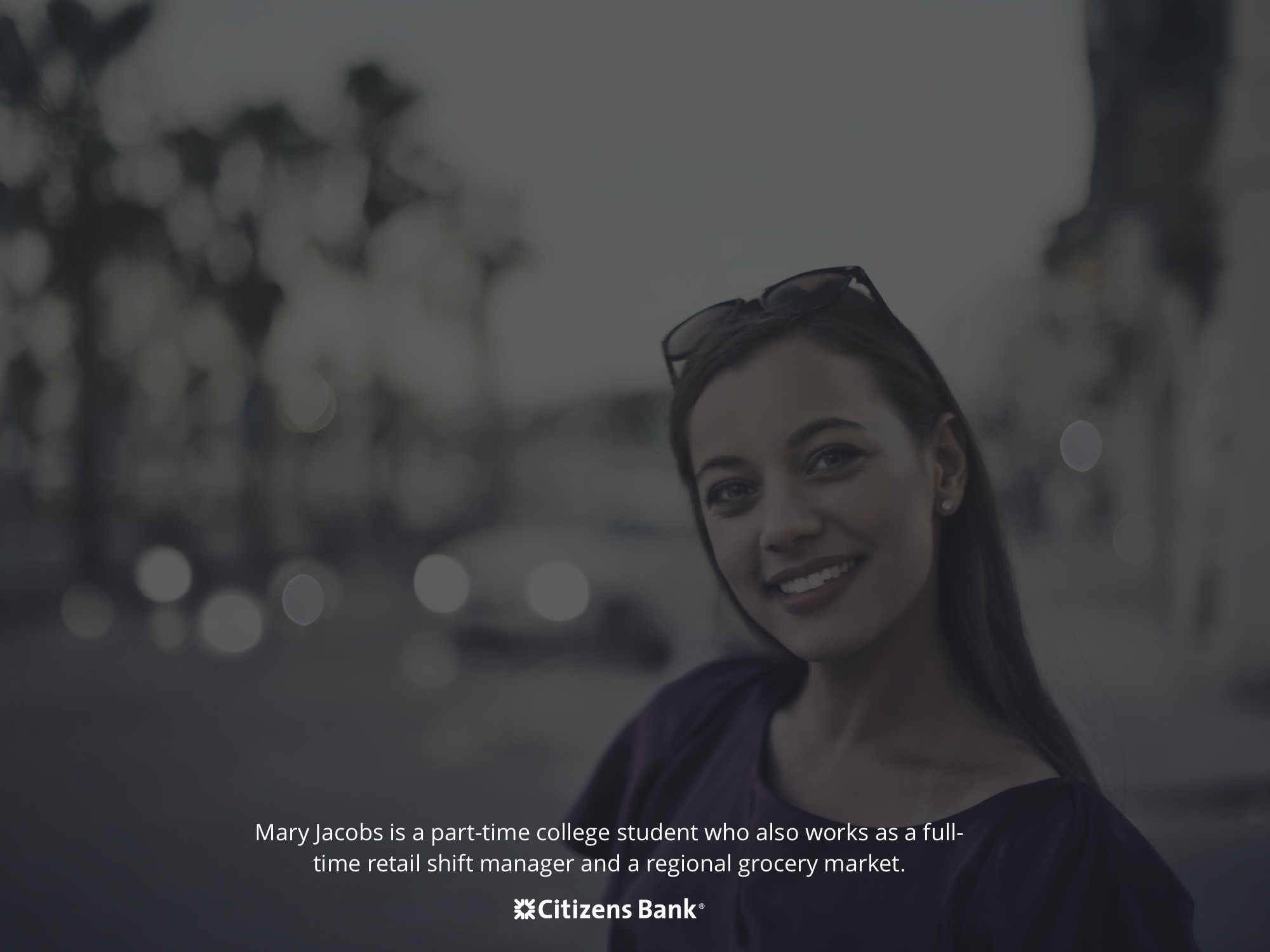

Meet Mary

To show the executive committee what a better experience could look like, I introduced a second persona. Mary Jacobs is a twenty-one year old part-time college student who also works full time as a retail shift manager at a regional grocery market chain. She lives in Providence and earns roughly thirty-five thousand dollars a year. She has had an accidental overdraft in the past, which is why she checks her balance carefully before almost every purchase.

Where Mike represented the acquisition opportunity, Mary represented the retention opportunity. She is a long-tenured customer whose trust in Citizens was inherited from her parents, and whose daily relationship with the app was already deep. If we could make her life easier during a moment of stress, we could protect a relationship that had been years in the making. The persona artifact captured her behaviors, frustrations, goals, and the financial products she already held with us.

Introducing Mary

Just as I did with Mike, I introduced Mary to the room with a single full-bleed photograph before I ever asked the committee to consider her financial life. The image shows a young woman in an urban setting, mid-laugh, unmistakably busy and unmistakably real. The caption grounded her in two sentences: she is a part-time college student who also works as a full-time retail shift manager at a regional grocery market.

That framing mattered. Mary is not a stock persona from a segmentation deck. She is the kind of customer our branches see every day, and her story was about to put a recognizable face on the retention risk the room had just acknowledged in part two.

Mary's Relationship With Citizens Bank

Mary has been a Citizens customer since the day she turned eighteen and graduated from high school. Her trust in the brand is inherited. Both of her parents banked with Citizens while she was growing up, and they had built real relationships with the tellers and bankers at their local branch. The staff greeted her parents by name every time the family walked through the door, and that memory is the reason Mary's very first checking account was with us.

I used this moment in the narrative to remind the room that retention at Citizens is not a spreadsheet line. It is a multi-generational trust asset that took decades to build and can be damaged in a single bad weekend. Any investment in this program was an investment in protecting that asset.

Mary's Vacation Plan

Mary has planned a vacation to Florida with her parents. Between her class schedule and her shifts at the grocery market, she rarely gets more than a few days away at a time, and this trip has been on her calendar for months. It is the kind of break that carries real emotional weight for a customer who works as hard as she does.

I chose to slow the narrative down on this slide on purpose. The committee needed to feel what was at stake for Mary before anything went wrong, because the failure scenario that followed would only land if they understood how much this trip meant to her in the first place.

What Mary Plans to Do While She Is There

Once in Florida, Mary is planning the kind of trip most customers would recognize. She will use Uber to get around because she does not have a car with her, she plans to do some light clothes shopping, and she is looking forward to a handful of bars and restaurants with her parents. None of this is extravagant. All of it depends on her debit card working the way she expects it to work, every single time she taps it.

This slide did an important piece of work in the narrative. It translated vacation into a list of small, specific card interactions that the executive committee could imagine themselves inside of. The product failure we were about to discuss would not be a single dramatic event. It would be a cascade of small moments that stopped working.

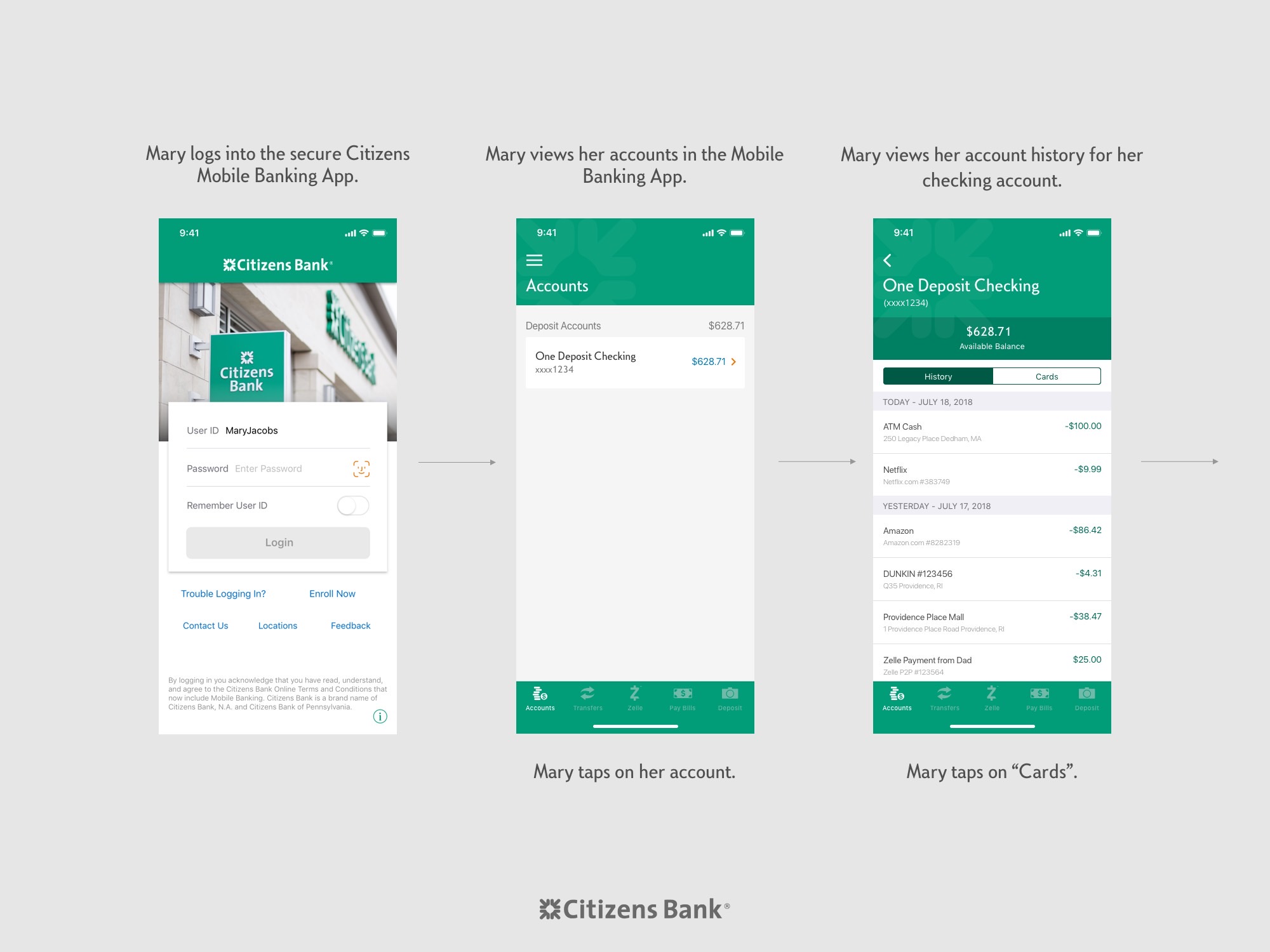

Logging In and Accessing Her Accounts

Before her trip, Mary logs into the secure Citizens Mobile Banking app, opens her One Deposit Checking account, reviews her recent activity, and navigates into the Cards section. None of this is new behavior for her. She is a customer who already checks her balance multiple times a week, and she expects to be able to reach anything she needs from the account screen in just a few taps.

I walked the committee through this flow slowly for a reason. Every feature that followed would be unlocked from this same screen. Making the navigation feel inevitable here set the stage for the rest of the Mary story to feel like a natural extension of the product she was already using, not a set of new tools bolted onto the side.

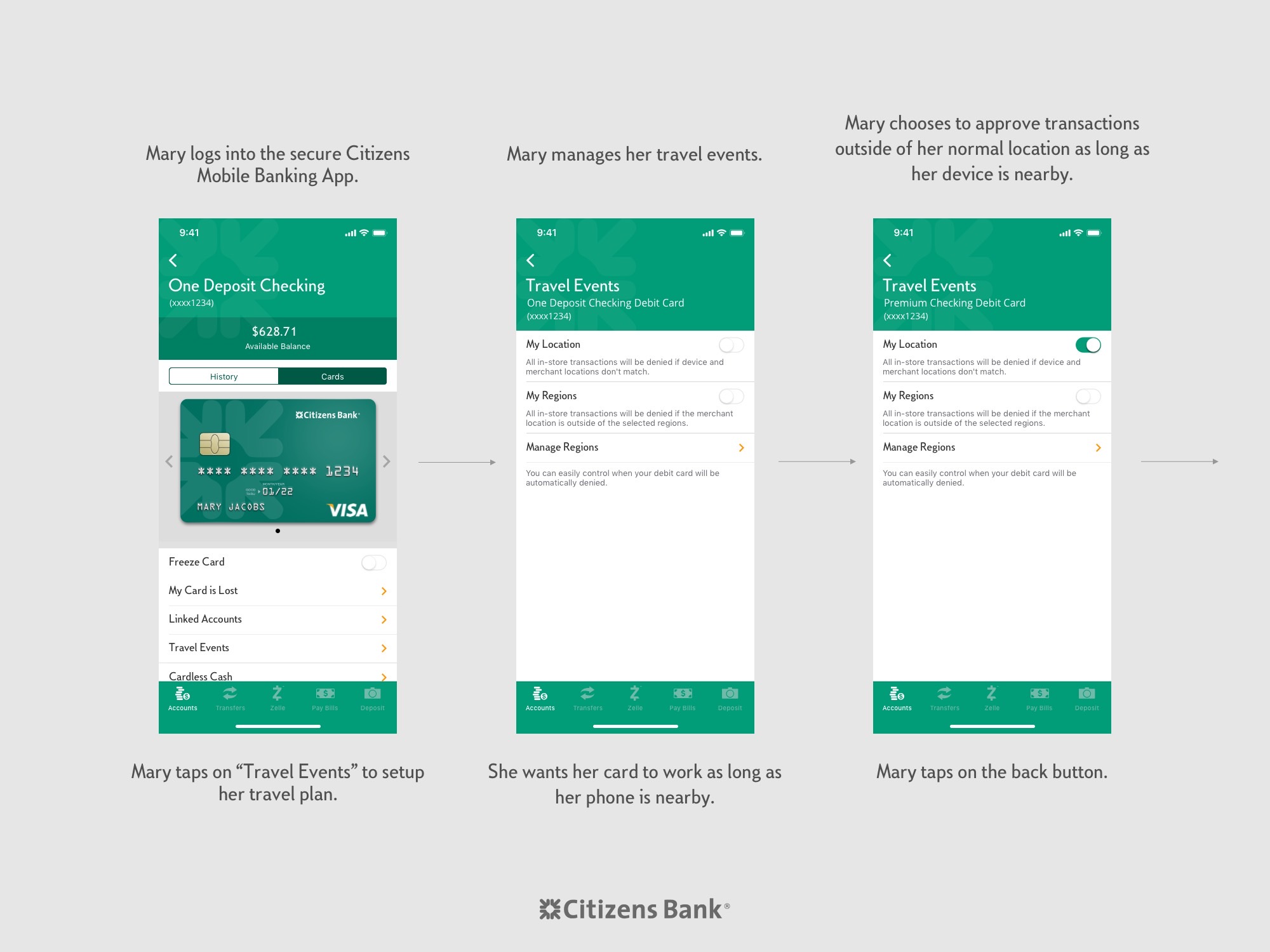

Setting Up a Travel Event in Card Controls

From the card controls screen, Mary taps into Travel Events and sets up a trip on her One Deposit Checking debit card. She tells the app where she is going, and she opts into a setting that lets her card work as long as her phone is nearby, so that transactions outside her normal location are approved automatically based on device proximity rather than being flagged and blocked.

This is the first feature in the narrative that directly answers the pain point we established in part two. The travel notification problem that caused a loyal customer to get stranded on vacation is solved by a control that Mary configures herself, in under a minute, without needing to call the bank or speak to a representative.

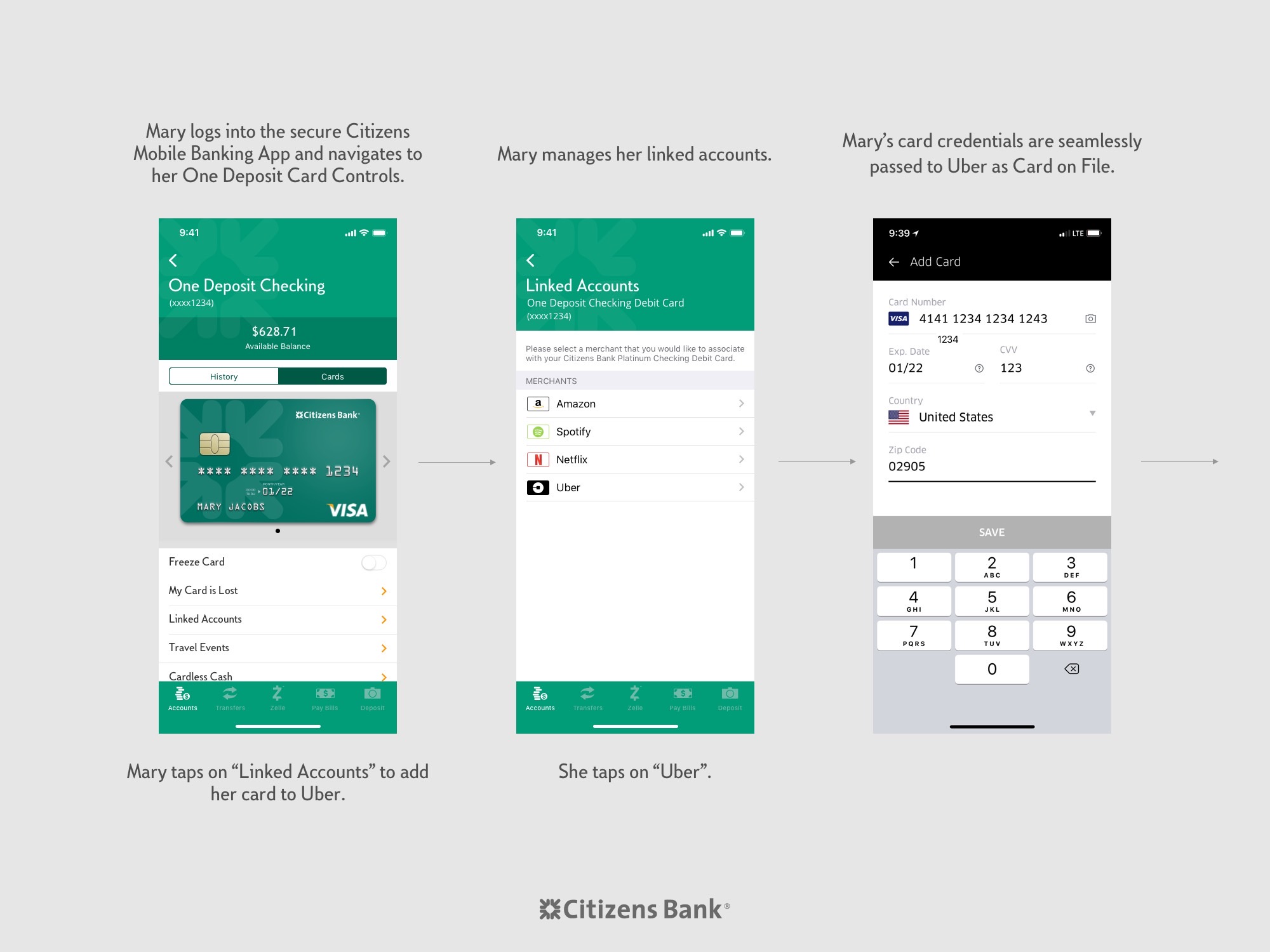

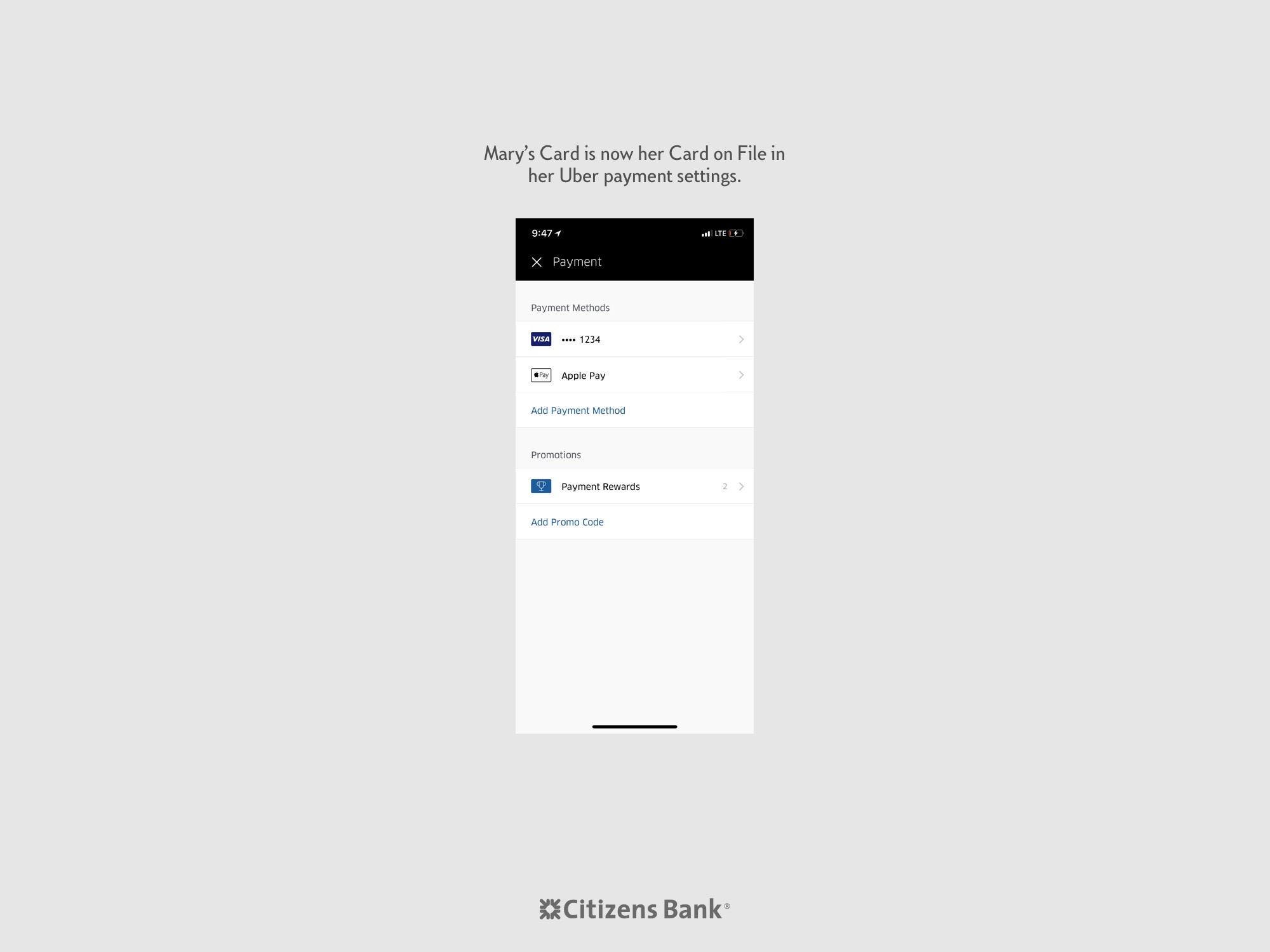

Linking Her Citizens Card Directly to Uber

Next, Mary navigates from card controls into Linked Accounts and taps Uber from a list of the merchants she uses most. With her permission, her card credentials are seamlessly passed from Citizens to Uber as a card on file, and the Uber app immediately recognizes her new payment method without Mary ever having to type a card number into a third-party surface.

This concept introduced a capability that genuinely excited the executive committee. It reframed the bank as an orchestration layer between the customer and the brands they use every day, rather than a passive source of card numbers. The value proposition was clear: a Citizens customer could update a card once, inside the bank, and have that update flow securely out to every service that relied on it.

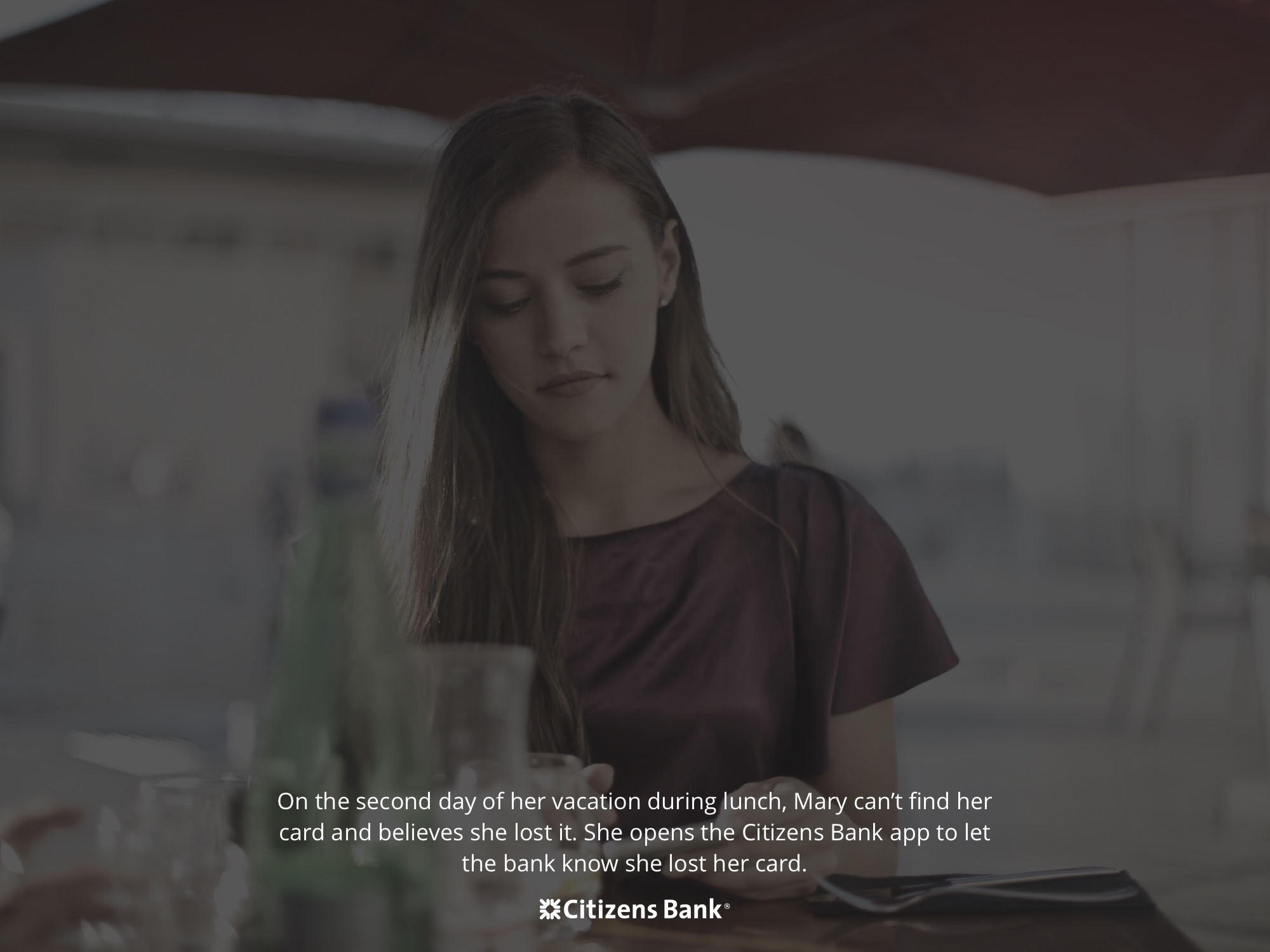

A Lost Card on Day Two of Vacation

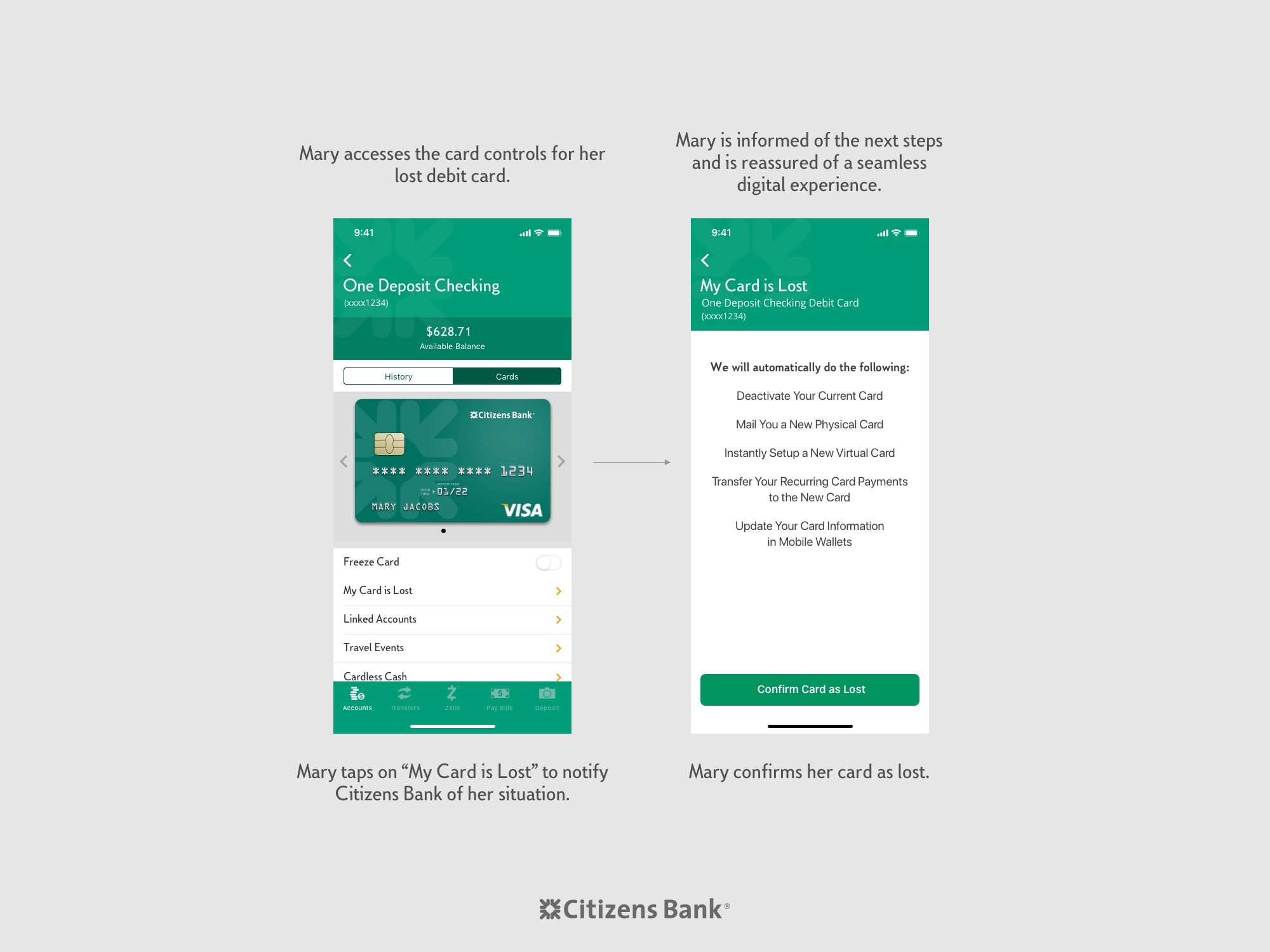

On the second day of her vacation, Mary sits down to lunch and realizes her debit card is gone. She does not know whether it slipped out of her wallet at the beach, fell between the seats of an Uber, or was left on a counter somewhere the day before. What she does know is that she is hundreds of miles from home, her parents are waiting on her for lunch, and the card she had been relying on for every purchase is missing.

She opens the Citizens Mobile Banking app directly from the table, navigates into the card controls screen for her One Deposit Checking account, and taps My Card is Lost. The app confirms her situation, then walks her through exactly what will happen next. Citizens will deactivate her current card, mail her a new physical card, instantly set up a new virtual card, transfer her recurring card payments to the new card, and update her card information everywhere it is stored in her mobile wallets. Mary taps Confirm Card as Lost, and the entire flow is done.

This was the moment the narrative pivoted from fear to relief. Everything that had taken days and multiple phone calls in the story from part two now took Mary less than a minute from a restaurant table on vacation. The executive committee could feel the difference, and they could see exactly which product capabilities their funding would pay for.

Back to Enjoying Her Vacation

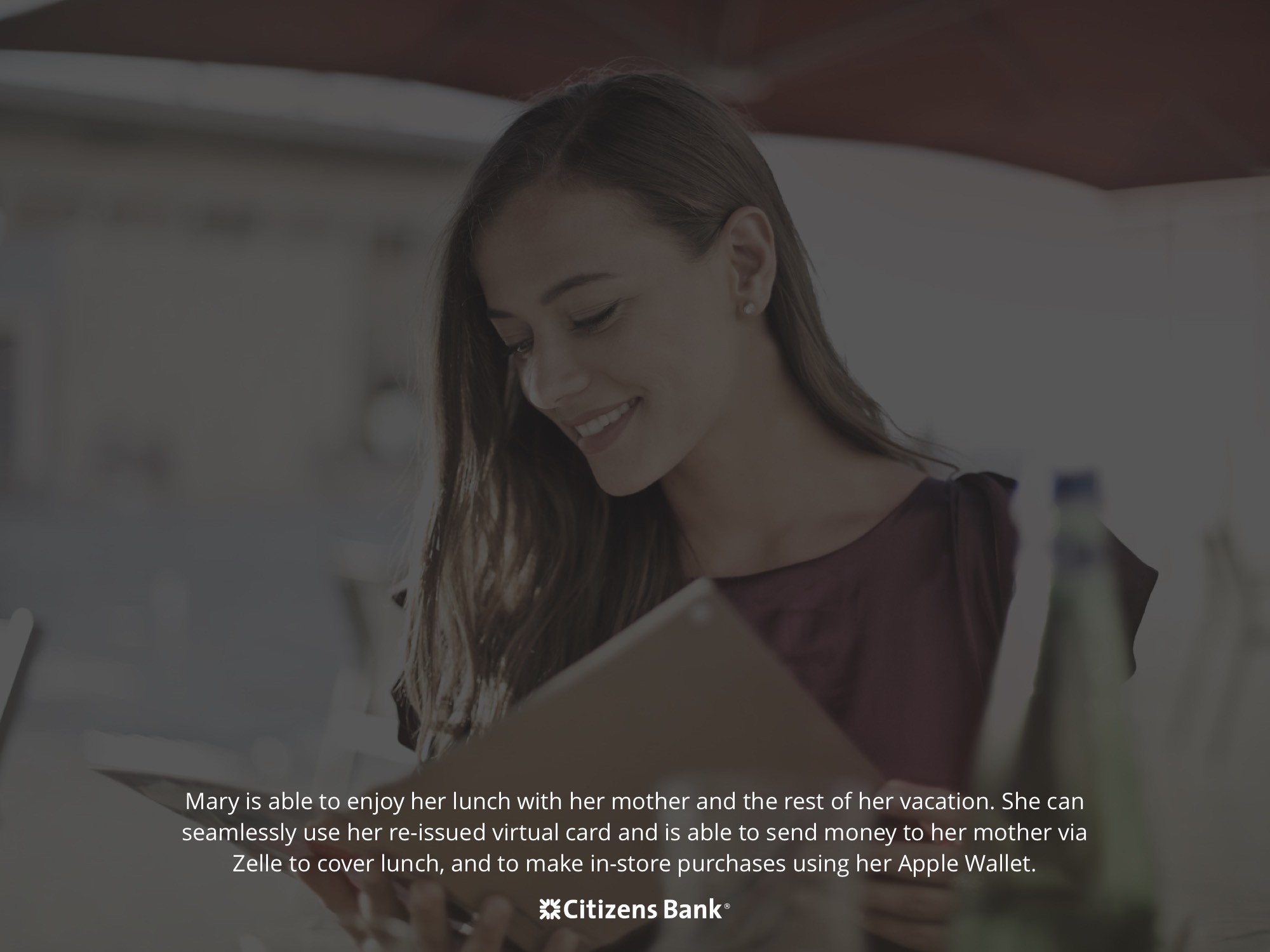

With her card reported lost and her new virtual card provisioned instantly, Mary goes back to doing what she came to Florida to do. She finishes her lunch with her mother, sends her mother money over Zelle to cover her portion of the bill, continues shopping with her new virtual card loaded into her Apple Wallet, and keeps taking Ubers without needing to touch her payment settings, because her card on file was updated automatically on her behalf.

The physical card that Citizens mailed to her home address will be waiting for her when she gets back. It simply does not matter anymore, because the product has already filled the gap. This final image closed the narrative on exactly the emotional note the presentation had been building toward. A loyal customer, on a trip she had been looking forward to for months, experienced a real setback and walked away with her day intact because of the work this program was asking to fund.

The Outcome

The visual storytelling framework did exactly what it was designed to do. By building a narrative around two customers the executive committee could see, empathize with, and recognize, the program stopped competing with other funding requests on the strength of its spreadsheet and started competing on the strength of its story. The room was no longer evaluating a product roadmap. It was deciding whether to leave Mike unsupported on day one and Mary stranded on day two of her vacation.

That reframing unlocked the investment. The presentation secured Tier-1 funding from the Consumer Bank and accelerated priority sign-off from the Head of Digital Banking, clearing the path for the Payments organization to move from strategy into delivery. Features that had lived as concepts on a backlog for months, including self-service travel events, instant virtual card reissue, linked merchant accounts, and real-time card-on-file updates, were now funded engineering commitments with executive sponsorship behind them.

Just as importantly, the approach itself became a reusable asset. Leadership walked away from the meeting with a clearer, more human understanding of the customers we serve, and the empathy-driven narrative format was adopted for future funding conversations across the Payments portfolio. A single well-told story did more than secure a single budget. It changed how the organization talked about the customer in the rooms where investment decisions get made.

Voice of the Customer

To make sure the room understood that the vacation scenario was not hypothetical, I pulled real social media feedback from actual Citizens customers who had lived through this exact experience. Each post surfaced a different facet of the same underlying problem: a blocked card at the worst possible moment, a replacement process that ignored the customer's physical location, and a support experience that forced the customer to do most of the work.

The slideshow below collects five of those customer voices. Use the controls to move between them and read each piece of feedback in their own words.

1 of 5